Structuring Overseas Property Ownership: Personal, Company or Trust?

Why Ownership Structure Matters

For many UK investors, buying abroad feels like a lifestyle choice — but the legal structure you choose defines how that asset behaves for decades.

The difference between holding property personally, through a company, or within a trust can affect:

- Tax efficiency (both UK and foreign)

- Succession and inheritance planning

- Privacy and control

- Access to finance

- Exposure to double-tax agreements

At Lucid Financial Markets, we help clients model these factors early — before contracts are signed — so ownership complements their wider wealth strategy.

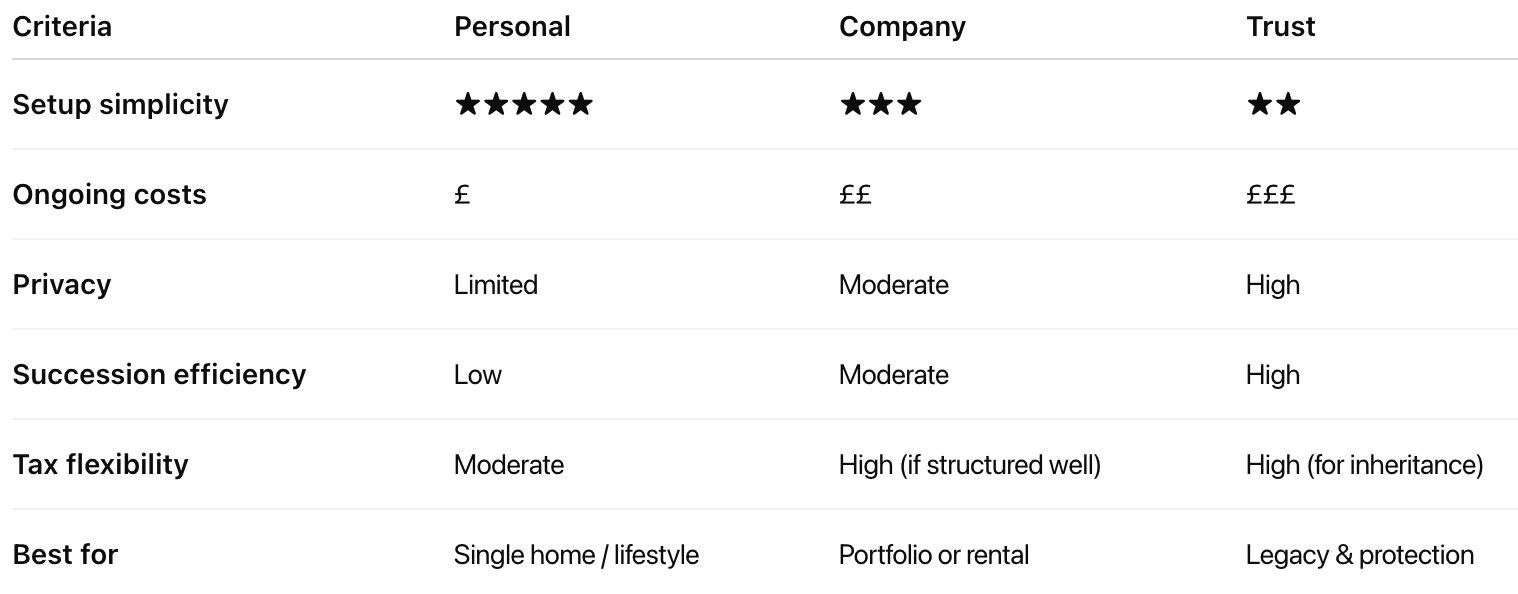

Option 1: Personal Ownership

✅ Advantages

- Simple to set up — purchase in your own name.

- Qualifies for certain reliefs (e.g. personal capital-gains exemptions in some EU countries).

- Straightforward financing and insurance.

⚠️ Drawbacks

- Full personal exposure to foreign tax and reporting.

- Potential double taxation on rental income or capital gains.

- Inheritance may trigger probate or cross-border legal delays.

Best for: Lifestyle buyers or single properties with limited rental activity.

Option 2: Company Ownership

✅ Advantages

- Corporate veil separates personal and property liabilities.

- May simplify joint ownership between family members.

- Easier to transfer shares than the property itself — efficient for succession.

- Potentially favourable treatment for business-use properties or portfolios.

⚠️ Drawbacks

- Ongoing compliance costs and foreign corporate tax filings.

- Some countries impose higher property taxes on corporate entities.

- Gains may face both local corporation tax and UK tax on dividends.

Best for: Investors with multiple overseas assets or those seeking long-term income generation.

Option 3: Trust Ownership

✅ Advantages

- Provides privacy and continuity — property held by trustees on behalf of beneficiaries.

- Useful for succession and estate planning across generations.

- Can integrate with broader wealth or family-office structures.

⚠️ Drawbacks

- Complex legal setup; requires professional administration.

- Some jurisdictions impose additional registration or disclosure requirements.

- Potential double taxation if not properly coordinated between UK and local law.

Best for: Families prioritising legacy and asset protection over short-term efficiency.

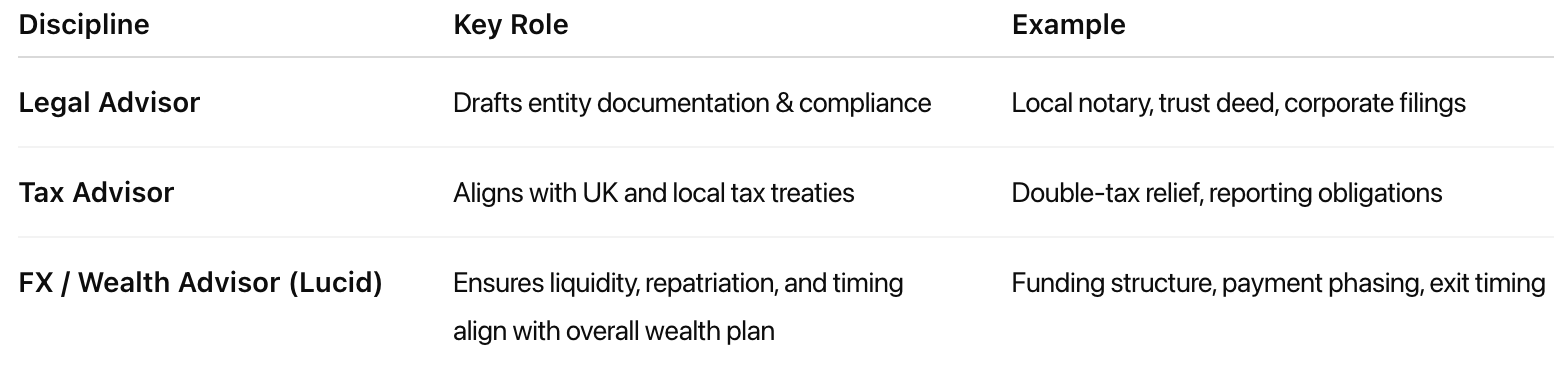

Cross-Border Coordination — The Lucid Framework

Effective structuring isn’t just a legal choice;

Lucid coordinates these moving parts so ownership, financing, and currency strategy operate seamlessly.

Comparative Overview

Lucid Insight

Ownership structure should never be an afterthought.

By assessing your tax position, intended use, and long-term objectives, Lucid helps you determine the optimal framework — not just for the property, but for your wealth ecosystem.

Key Takeaways

- Structure drives both tax outcomes and family continuity.

- Personal ownership is simplest; trusts and companies bring flexibility but complexity.

- Always integrate legal, tax, and FX planning — they operate together.

- Review structure annually as tax treaties evolve.

If you’re considering a property purchase abroad, speak with a Lucid Advisor before finalising your ownership structure.

We’ll coordinate with your legal and tax partners to ensure your property fits neatly within your long-term financial strategy.

We help...

Here's What Our Private and Corporate Clients Said

“Relocating overseas meant moving significant funds, and Lucid handled it flawlessly. Dave's personal approach, clear communication, and excellent rates gave us full confidence throughout. We saved a substantial amount compared with our bank and genuinely felt looked after from start to finish.”

“We used Lucid for a large currency transfer linked to our villa purchase in Spain. David and his team made the process effortless, kept us informed at every stage, and locked in a fantastic rate. The experience was far more reassuring than dealing with the banks — highly recommended.”

''David was very detailed about the service, kind in his communication, engaging as a person, and helpful with as much as he could. I really enjoyed working with him and I feel like I've made a long-term connection.''

''I have used a range of online FX services before (Wise, etc...). I was introduced to Lucid as I needed to do a number of higher value transactions.David has been brilliant: transparent, available, good advise,...Overall great service and value for money. Highly recommended and would use again.''

''I used Lucid / David for a purchase of a property in Spain. Was a very good service and would recommend. It's pretty stressful transferring large sums cross border and David gave a very good personal service.''

.svg)

Our take

Empowering financial decisions for corporate and high net worth clients through currency risk management and best execution.

© 2025 by Lucid Financial Markets.