Spain, Portugal, Italy or Majorca? Choosing Your Second-Home Market Through a Wealth Lens

Introduction

For many UK families, a second home in southern Europe represents more than a lifestyle dream; it’s a long-term wealth decision.

Yet choosing where to buy — Spain, Portugal, Italy or Majorca — requires balancing lifestyle goals with the realities of taxation, financing, and future liquidity.

At Lucid Financial Markets, we help private clients view cross-border property through a financial lens, integrating ownership decisions into wider wealth and succession planning.

🇪🇸 Spain — Established, Efficient and Highly Liquid

Market Snapshot

- Largest and most transparent of the southern-European markets.

- ~300 000 UK homeowners; strong resale activity.

- Popular zones: Costa del Sol, Costa Blanca, Barcelona, Balearics.

Tax & Ownership

- Acquisition tax: 6–10 % (regional).

- Annual IBI: ≈ 0.4–1.1 % of cadastral value.

- Rental income tax: 19 % (EU resident).

- CGT: 19–23 %.

Predictable but not low-tax. Spain suits buyers prioritising lifestyle stability and liquidity over optimisation.

Financing

- Non-resident LTV ≈ 60–70 %.

- Euro fixed-rates still attractive for long holds.

Exit View

Strong secondary market and deep demand ensure smoother disposals.

Planning ahead for regional taxes and notary timelines is essential.

🇵🇹 Portugal — Tax-Smart and Investor-Friendly

Market Snapshot

- Lisbon, Porto, Algarve remain prime.

- Prices ≈ 20–30 % below equivalent Spanish resorts.

- Increasing interest from digital professionals and retirees.

Tax & Residency

- No wealth tax; no inheritance tax for close family.

- CGT: partial exemption after 2 years ownership.

- NHR regime (phasing out but legacy benefits remain) offered 10-year foreign-income relief.

Forthcoming “Talent” incentives keep Portugal appealing to internationally mobile clients.

Financing

- LTV ≈ 65 %, conservative underwriting.

- Euro loans with early FX planning provide predictability.

Exit View

Urban & coastal areas liquid; rural locations slower.

Repatriation timing matters — sterling strength can magnify returns or erode gains.

🇮🇹 Italy — Legacy and Lifestyle Value

Market Snapshot

- Heritage markets: Tuscany, Lake Como, Rome, Milan.

- Demand driven by culture and family legacy rather than yield.

Tax & Residency

- €100 000 flat tax on foreign income for HNW residents.

- No wealth tax on worldwide assets.

- Acquisition tax ≈ 9 % (second home).

Financing

- Lending tight; many cash purchases.

- Local banks prefer resident income or domestic collateral.

Exit View

Longer holding periods required; capital appreciation steady but slow.

Excellent for inter-generational planning and lifestyle diversification.

🇪🇸 Majorca — Exclusive Island Liquidity

Technically part of Spain yet operating as a distinct micro-market.

Market Snapshot

- Strict building controls and limited supply support price resilience.

- Palma and south-west coastal areas lead luxury transactions.

Tax & Costs

- Same as mainland Spain but property values higher; buyers face 8–11 % total purchase costs.

Financing & Exit

- Access to Spanish lending network.

- Liquidity strong for prime villas — international buyer base diversified across Europe and US.

Wealth View

Low supply and strong rental demand make Majorca a premium preservation asset rather than a yield play.

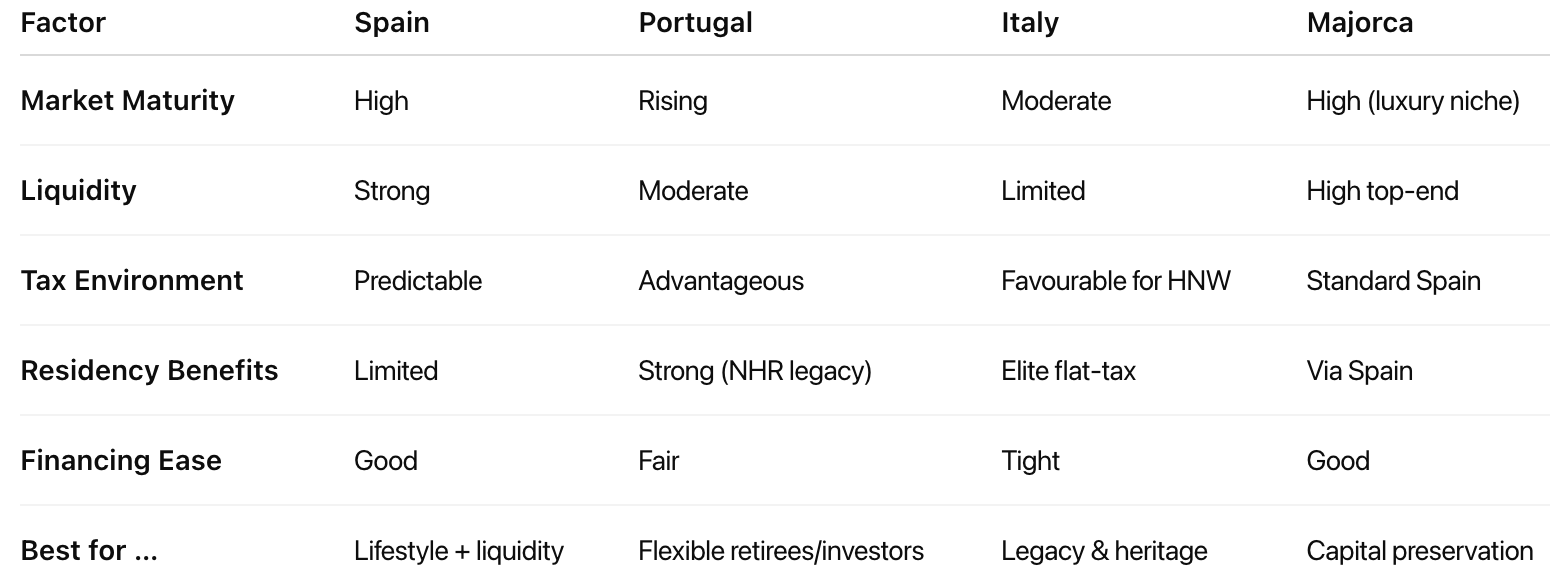

Comparative Summary

Lucid Insight: Align Emotion with Economics

Each market can serve a different role within a private client’s portfolio.

- Spain: balanced liquidity and lifestyle — a classic base for regular use.

- Portugal: agile tax environment — optimised for cross-border income.

- Italy: depth and heritage — ideal for family legacy and residency.

- Majorca: exclusivity and stability — a store of value for global families.

The right choice depends on how you intend to fund, use, and ultimately exit the property — not simply where you’d like to holiday.

At Lucid Financial Markets, we combine property insight with structured FX, tax, and liquidity planning so clients can make informed, wealth-aligned decisions across Europe.

Speak with a Lucid Advisor to design your European second-home strategy with clarity and control.

We help...

Here's What Our Private and Corporate Clients Said

“Relocating overseas meant moving significant funds, and Lucid handled it flawlessly. Dave's personal approach, clear communication, and excellent rates gave us full confidence throughout. We saved a substantial amount compared with our bank and genuinely felt looked after from start to finish.”

“We used Lucid for a large currency transfer linked to our villa purchase in Spain. David and his team made the process effortless, kept us informed at every stage, and locked in a fantastic rate. The experience was far more reassuring than dealing with the banks — highly recommended.”

''David was very detailed about the service, kind in his communication, engaging as a person, and helpful with as much as he could. I really enjoyed working with him and I feel like I've made a long-term connection.''

''I have used a range of online FX services before (Wise, etc...). I was introduced to Lucid as I needed to do a number of higher value transactions.David has been brilliant: transparent, available, good advise,...Overall great service and value for money. Highly recommended and would use again.''

''I used Lucid / David for a purchase of a property in Spain. Was a very good service and would recommend. It's pretty stressful transferring large sums cross border and David gave a very good personal service.''

.svg)

Our take

Empowering financial decisions for corporate and high net worth clients through currency risk management and best execution.

© 2025 by Lucid Financial Markets.